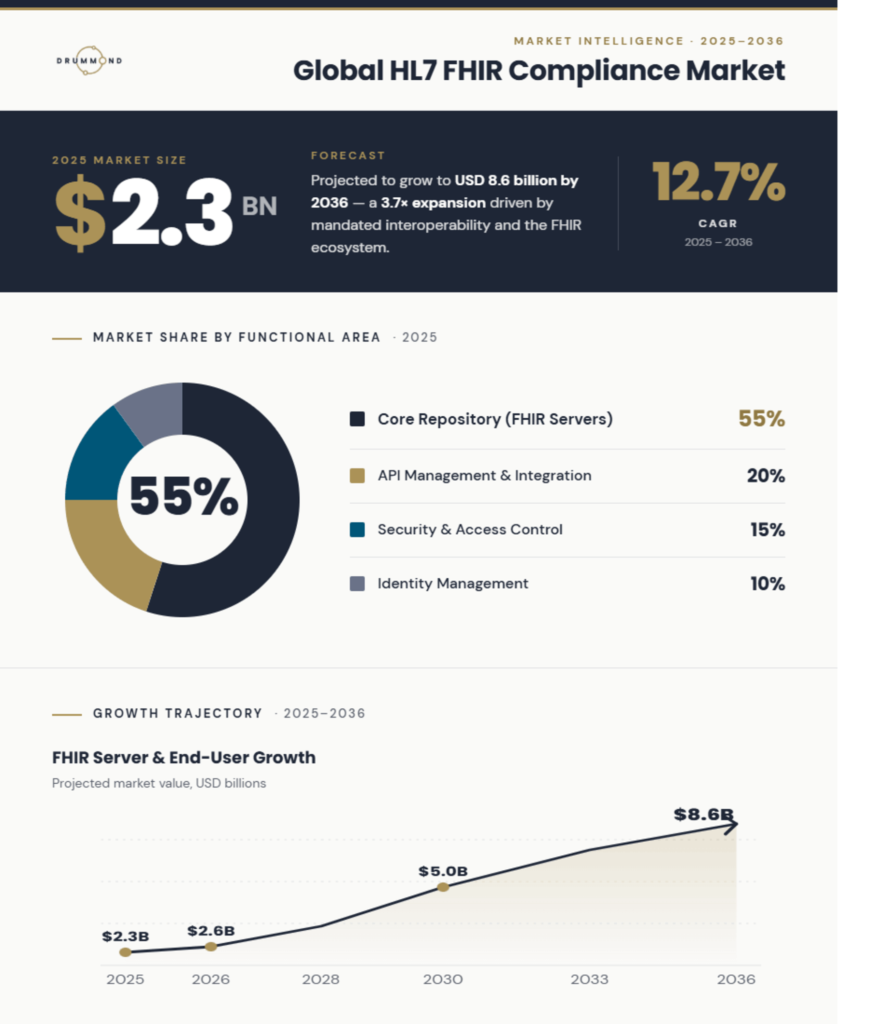

Future Market Insights (March 2026) valued the global HL7 FHIR compliance market at $2.3B, with projections reaching $8.6B by 2036 (12.7% CAGR). The analysis named Epic, Oracle Health, Microsoft, and Redox among the key players driving that growth. Drummond was recognized alongside them for its role in independently validating FHIR implementations through FHIRplace.

That recognition reflects a FHIR market already in motion. The market growth projection is not just a future outlook, but a signal of accelerating regulatory and implementation activity.

FHIR compliance is shifting away from being a technical checkbox and toward a baseline expectation embedded in how buyers evaluate potential partners.

Three forces are driving that shift, and they are not moving independently. They are converging. Organizations that understand what is behind this transition will be best positioned to move ahead of it.

Those that do not will find themselves reacting to a competitive environment that is already shifting faster than their ability to adapt.

Three Forces Compounding the Market

Regulatory Pressure

Federal regulatory pressure is the most visible force. The CMS Interoperability and Prior Authorization Final Rule requires impacted payers to implement FHIR-based APIs by January 1, 2027. Operational provisions, including faster prior authorization decision timelines and metric collection, took effect January 1, 2026, with the first public reporting of PA metrics due March 31, 2026.

The deadlines are clear, and their impact is already showing how payers are investing and planning implementations.

What remains unsettled is how performance will be judged once systems are operating across real partners, real data exchanges, and real scrutiny. That uncertainty is quietly influencing investment just as strongly as the deadlines themselves.

Regulatory requirements specify what to build. They are less prescriptive about how to prove it works across a real and varied partner network. What counts as demonstrated interoperability in one procurement context may not satisfy the next.

That gap between compliance on paper and validated performance in production is where interpretation varies, and leading organizations are not waiting for greater clarity to emerge. They are investing in how to build robust interoperability they can rely on, rather than risk it falling short when it has to be proven in real-world use.

Structural Changes to the FHIR Ecosystem

The structural force is a direct contributor to the market investment the FMI projection describes. Regulatory mandates are not just setting deadlines; they are expanding the ecosystem itself. Every organization required to implement FHIR-based APIs under CMS-0057-F becomes a new node in a network that every other participant now must connect with. As more payers, providers, health information exchanges, and government agencies come online, the matrix of connections every organization needs to build and maintain grows.

Each new partner brings its own systems, its own upgrade cycles, and its own interpretation of implementation guides. Managing each connection with one-to-one integration projects is not scalable. When a single partner updates their system the integration needs revisiting. Multiply that across twenty or fifty partners each with their own independent timelines and the scaling burden alone justifies increased investment in implementation and integration.

The FMI analysis reflects this directly. Implementation and integration services account for roughly 45% of FHIR compliance market spending as organizations require ongoing support to manage mapping, validation, and governance across a partner ecosystem that never stops changing. Those investments do not decrease as the market matures; they grow with it.

The Market Is Setting Its Own Bar

The third force is different in nature from the first two. Regulatory mandates are imposed from outside. Structural complexity is created by growth itself. The third force comes from within the market. As FHIR adoption accelerates and more organizations demonstrate real-world interoperability readiness, the standard for what it means to be a credible integration partner shifts, not because a regulator moved it, not because the ecosystem grew more complex, but because participants in the market have already shown what production-ready looks like.

That creates a new kind of pressure. When enough organizations in a market demonstrate a higher standard of readiness, that standard stops being exceptional and starts becoming the norm. Elevated expectations drive continued and expanding investment in FHIR capabilities to keep pace with the market.

All three forces point to the same conclusion. Organizations are investing in FHIR, pursuing certification, and working toward upcoming deadlines. That investment reveals a widening gap in how readiness is actually understood and achieved. However, the gap that emerges is not between organizations that are willing to satisfy FHIR requirements and those that are not.

It is between organizations that understand what true FHIR readiness requires and those that have mistaken compliance for actual readiness.

In a Booming Market, Compliance Is the Entry Ticket

Compliance and interoperability are not the same thing. Compliance confirms that your implementation meets the specification. Interoperability confirms that it works in production, across the real systems your partners are running. Treating one as a proxy for the other is the most common way organizations get left behind.

The financial cost of confusing them is concrete. A FHIR implementation that passes every compliance check can still break in production when it meets a partner that interprets an optional field differently, maps a procedure code through a different clinical terminology, or structures data upstream in a way the specification never anticipated.

FHIR is deliberately flexible. The standard allows significant variation in how optional fields are used, how implementation guides are interpreted, and how coding systems are applied across different organizational contexts. That flexibility is what makes broad adoption possible. It is also what makes controlled-environment testing an unreliable proxy for production readiness.

Internal tests validate your system against your own assumptions about how partners behave. Those assumptions diverge from reality every time a partner makes a different implementation choice.

In a stable ecosystem with a small partner count, the cost of those limitations is manageable. In a market growing at 12.7% annually (more partners, more integration surface area, higher commercial stakes on every connection) each production failure that was not prevented with compliance testing costs more than it did the year before. Partner relationships are harder to repair at scale. Engineering resources are more expensive to divert. Delayed go-lives carry larger opportunity costs as the market moves faster around you.

Chasing compliance in this environment does not maximize ROI. It defers the cost of insufficient testing to the moment when it is most expensive to absorb.

For a deeper look at the technical limitations of compliance-only approaches to FHIR testing, read our blog on why traditional QA is reaching its limits in FHIR ecosystem testing.

What Validated Interoperability Returns in a Growing Market

The healthcare organizations best positioned in an expanding FHIR market are not the ones that reached compliance and stopped. They are the ones that treated interoperability as an ongoing operational capability and built a track record of demonstrated, real-world readiness.

For providers, the return runs through patient satisfaction. When prior authorization requests fail or return incomplete data, care is delayed. Patients waiting on approvals for procedures, medications, or referrals experience those delays directly. In a market where patient experience scores influence reputation, referral volume, and value-based care contract performance, moving patients through authorization workflows quickly is not a clinical nicety. It is a revenue driver.

Providers that process prior authorizations faster, with fewer failures and less manual intervention, retain patients, strengthen payer relationships, and perform better against the reimbursement metrics that value-based models use to determine payment.

For payers, the return is network efficiency. A payer that connects to new providers quickly, processes prior authorization requests without data failures, and exchanges clean clinical data across a growing network spends less on manual intervention and exception handling. In a market where payers compete to build broader, higher-quality provider networks, onboarding providers without friction is a direct input to network strength and member retention.

For health IT developers, the benefit is simple: faster time to market and lower engineering cost. Testing against real partner systems before deployment helps catch compatibility issues early, when fixes are quicker and cheaper—, instead of after go-live, when they take more time, strain partner relationships, and delay expected revenue.

Post-deployment issues do not just add operational cost. They also disrupt the roadmap, pulling teams back into work they thought was finished and delaying what comes next.

Organizations participating in structured, real-world testing now will enter the coming compliance period with something no amount of last-minute preparation can produce: a documented history of interoperability testing across real partner systems.

Build for the Market Ahead

The FHIR compliance market is projected to be nearly four times its current size by 2036. The regulatory requirements driving that growth are not hypothetical. The partner ecosystem expanding that demand is not slowing down. The commercial pressure to prove interoperability readiness before contracts are signed is already operating in the market today.

What the $8.6 billion projection actually describes is a market that has moved past the question of whether FHIR interoperability matters. The question every organization now faces is whether their testing approach is built for the ecosystem they are operating in or the one they were operating in two years ago.

FHIRplace exists for organizations that want a clear answer to that question. It is a Drummond-managed testing environment where health IT developers, payers, and providers validate their implementations against real partner systems, not controlled environments, not mock servers, and not theoretical conformance assessments.

The result is documented evidence of real-world readiness built before requirements arrive, not assembled under pressure after they do.